How founders should think about runway: A guide from Sequoia Capital. | VC & Startup Jobs.

Founders: stop saying these things in VC meetings. Don’t price your product based on costs.

👋 Hey, Sahil here! Welcome to this bi-weekly venture curator newsletter, where we dive into the world of startups, growth, product building, and venture capital.

FROM OUR PARTNER: ZOOM

⌛ When was the last time you worked just 8 hours in a day?

Be honest. Most of us are clocking 10, 12, or even 14 hours—and still ending the day feeling behind. It’s not always the hard stuff that drains you. It’s the little things around the work that quietly steal your time:

Manually tracking hours after every call

Writing follow-up emails that were supposed to "write themselves"

Sending calendar links back and forth

Playing assistant, note-taker, and project manager all at once

If you’re putting in long hours, every minute should count. The fix isn’t more time—it’s smarter tools that handle the overhead for you.

Imagine this:

Your meeting notes write themselves

Hours get logged automatically while you talk

Scheduling happens without the back-and-forth

You don’t need more hours. You need better tools.

In today’s newsletter -

Deep Dive: How founders should think about runway: A guide from Sequoia Capital.

Quick Dive:

Founders: stop saying these things in VC meetings.

Do Early-Stage startups need a financial model for fundraising?

Don’t price your product based on costs, why?

Major News: Coinbase CEO's new biotech startup raises $130M, OpenAI to reduce Microsoft revenue share after restructuring, OpenAI abandons plan to become a for-profit company & Microsoft has officially discontinued Skype.

20+ VC & Startups job opportunities.

📬 VENTURE CURATORS’ FINDING

My favourite finds of the week.

VC is full of people from all over the place - Tech, non-tech, consulting, non-operators.

Why o3 is the best model yet for real-world learning.

Post-election shift in web3VC by Tomasz Tunguz.

Startup legal document pack – essential legal docs for founders.

Why I Invest in venture funds by Product Hunt founder Ryan Hoover.

How to ship 10x faster.

This is the only startup valuation guide you need as a founder.

Investor network across the hottest 100 AI companies.

400+ French angel investors & venture capital firms contact database (Email + LinkedIn Link)

Need a pitch deck that gets investor meetings? We’ve opened just 3 slots to help founders craft winning decks—built by experts, and reviewed by investors. Don’t leave funding to chance—[schedule a call today →]

📜 TODAY’S DEEP DIVE

How founders should think about runway: A guide from Sequoia Capital.

Founders often view runway as just a number or equation, but VCs expect them to think beyond that. Sequoia Capital shared a framework on how founders should approach the runway. In this write-up, we will discuss...

Runway Reality

What is your runway right now? How should you calculate it?

How should you think about how much runway you need?

How do you extend your runway if you need more?

Let’s deep dive into this….

The basics: What is a runway?

It’s your cash balance divided by your monthly burn.

If you have $10M in cash and $0.5M in burn, you have 20 months of runway

But it gets a little more nuanced than that. The cleanest way to look at your cash balance is net cash, which is the cash you have on your balance sheet minus any debt you’ve drawn.

If you have $10M in cash but you’ve drawn $5M in venture debt, you really have $5M of net cash and you should use that number to think about your runway.

But why? The reason is that debt is borrowed money. It’s not yours. You owe it to a creditor. Similar to how you make personal budget decisions based on your assets minus whatever debt you owe, you should think about your company’s cash position the same way.

The TLDR is that having a line is a helpful lifeline when you’re facing a cash crunch, but drawing it comes at a cost. It makes it harder to raise your next round. It comes with covenants which means debt holders can own more and more of your company. It can be a negative signal, and it can generate a lot of overhangs.

That said, one of our recommendations, if you are tight on cash, is to secure a venture debt line and just not to consider it part of your runway. Ideally, you don’t draw on it unless absolutely necessary, with eyes wide open to the tradeoffs

Monthly burn—this is different from your net income.

Net income is an accounting concept. Burn is cash in minus cash out.

It takes into account things that aren’t in your monthly P&L: for example, if you have to buy inventory upfront, or if you have capex outlays upfront, or for a subscription company if you collect upfront on yearly contracts—all of these things impact your cash burn. It’s critical to have a very tight grip on what your cash burn is. There may be ways to reduce the gap between EBIT and free cash flow—maybe that means paying your suppliers a little later or collecting revenue earlier.

If you have a lumpy business, meaning you have to provide cash upfront to build out capital expenditures or you’re purchasing inventory, it’s existentially important to have a very detailed understanding of your expected cash outlays. If you’re not careful in managing and forecasting these outlier expenses, then your runway can turn out to be 3 months when you thought it was 15.

One more thing: Runway is not static.

Just because you have 8 years of runway doesn’t mean you can forget about it and assume you’re fine. As your revenue and expense base change, your runway can change very quickly. You want to stay focused on the burn number. You should be calculating your runway every single month and watching that number religiously.

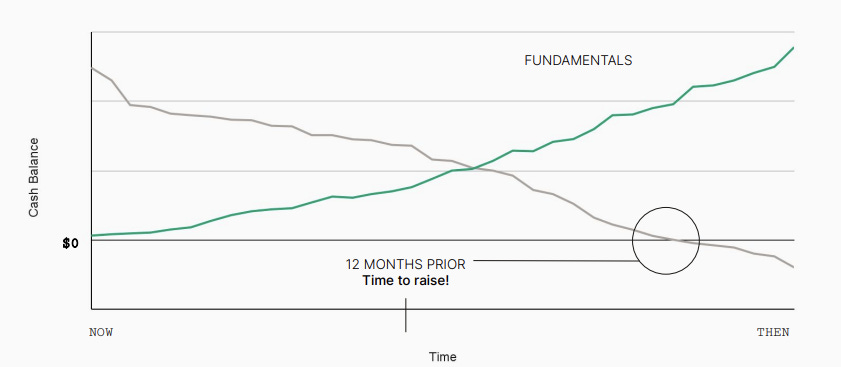

A Mental Framework For Founders - Runway and Milestone

If you are reading this newsletter, previously I have mentioned “You are raising fund not to increase your runway, but to achieve your milestone”

As a founder, how should you look at this graph? Suppose you and your CFO put your heads together, and your best guess for how cash changes over time looks something like this chart.

This is your cash-out point. 12 months before that, it’s time to think about raising again.

Runway doesn’t come in a vacuum. It’s intimately tied to meeting valuation milestones.

Imagine you’re driving your car on the freeway and running out of gas. What matters is not how many gallons of gas you have in your car, but whether it’s going to last you until you reach the next gas station. Think about what your goal is for your next fundraising. Maybe it’s an up round. Maybe it’s a flat round. Maybe it’s a down round. Maybe it’s to reach a cash flow positive.

Whatever your goal is, which is a conversation between the leadership team and the board, there is some valuation milestone attached to achieving that goal. Figure out what metrics or “fundamentals” get you to your goal. Maybe it’s ARR. Maybe it’s Gross Profit. This is the green line on this chart.

The rough mental framework is that well before you run out of cash, you need to make sure you have the fundamentals in order to meet your next valuation milestone.

These two lines are intertwined (Previous image). There’s a delicate balance in your scenario analysis between investing in growth and burning cash in order to make sure that you are leaving enough runway to meet the next milestone. It’s important to hope for the best but plan for the worst as you are plotting out how to make the math work.

Raising your next round on pure story is not enough anymore.

That worked when the capital was plenty, but investors are now going to care about your metrics, and more importantly your financials. So it’s important to make sure that you are focused on getting that valuation milestone to the right place.

Now, you’ve done the exercise of figuring out your runway versus your metrics and valuation fundamentals. There are three possible scenarios for your runway situation:

Bucket 1: <12 months of runway, when it is existential to focus on your runway

Bucket 2: 12 months of the runway but not enough to raise a flat round based on rational metrics: Here it’s critically important to focus on the runway.

Bucket 3: Enough runway to raise a flat round, up round or reach cash flow positive: Stay the course and continuously optimize.

Some founders are in Bucket 1. A few are in Bucket 3. But many are in Bucket 2. If we can emphasize one point in this writeup it’s this: many founders may think they’re in Bucket 3 but are actually in Bucket 2.

The financials that you have to reach to cover your next round have changed. The bar has been raised. Many of us are 3-4 years away from reaching our last valuation, with less than that amount of cash. In that case, it’s critically important to focus on managing the runway, even if you have years of runway remaining.

So - how to extend your runway?

If you take us at our word that all probably need more runway than thought, the question is: How do you get it?

Like many things in business, it's very easy to say and it's very hard to do.

The first step in getting very tactical is to understand your current state.

This means looking deeply into your P&L. If you're talking about runway, that means you're losing money every month. So you have to figure out where the net loss comes from. Once you’ve identified the specific places in your P&L causing your burn, you can start thinking about which dollars yield efficient growth and which are not as helpful

To understand which parts of your P&L need to be addressed, begin with the big picture and break it down into parts. Starting with net loss, you can break that into two parts: gross margin and opex.

Then break each of those down into component parts: ○ What are all the drivers of your gross margin? What is the cost of sales, etc? ○ What are all the drivers of compensation opex and non-compensation opex? How much of the opex is dedicated to computer hardware, hosting and subscriptions, etc? ● Keep breaking it down until you have a detailed view of the components that contribute to total net loss.

Once you’ve identified the important contributions to your burn, you can plot them in terms of their burn impact on the y-axis. Then there’s the ease of execution:

how easy is it to address and how big an impact does it have? Unfortunately, you’re not likely to find many items that are high-impact and easy to execute. Changes that extend your runway a lot will almost certainly be difficult. This plot is important because it will set your roadmap for the actions you take to extend your runway

Once you understand the levers available to impact the runway, you can use them to set a goal. Your goal should be oriented around how long it’s going to take for you to reach a rational milestone. Let's say your goal is a flat round. Given the market conditions, for many of us that’s going to take us three years.

To unpack why that is:

Say you hypothetically raised your last round at a billion dollars, and you have five to 10 million of ARR.

if you want to raise your next round at a billion dollars, you might need 75 to 100 million of ARR, which might mean you need to grow about 10 to 15X.

It takes time to do that. It very well might take three or four years

If it takes three years, recommend you have four years of runway. The reason: as mentioned earlier, you want to raise 12 months before running out of money. Generally, investors view it as a bad sign to have a very short runway, so you want to avoid being in this situation when raising a round. So the time you need to hit your goal plus 12 months is the ideal runway that would suggest.

One recommendation: When you decide how long it will take to reach your goal, be very realistic. Use public comps and ask the toughest board member. Ask her what it will take to reach a flat round based on rational milestones, and then add 12 months.

So now you've taken the steps to understand where you are, and you’ve broken down your P&L to understand where the money goes. You've plotted your options in terms of ease-to-execute versus burn impact. And you’ve set a goal based on rational milestones.

So let's say hypothetically you need to cut your burn from $3 million a month to $2 million. We don’t want to sugarcoat this: It's going to be hard. Of course, a people-related cut is the hardest decision any leader makes. Beyond this, you may face many challenging and nuanced decisions:

If you're a global company, you might need to reevaluate certain markets.

If you're a company that's relied on a marketing or sales investment in order to grow, you might have to reevaluate your strategy.

You might have to increase pricing. This is scary, especially if you don’t have time to fully test the value proposition.

The big thing to remember is this: If you take the steps necessary to extend your runway in line with rational milestones, confident you and your whole company will be better on the other side.

So Overall :

You likely need more runway than you think.

Ultimately, your next round will be based on your metrics, which is going to be reflected in your financials.

Be real about what bucket you're in. Think most companies are in Bucket 2, which is more than 12 months of cash, but need to make some changes.

You have what you need to win. You can execute and we're here to help you do that

INSIDE VC: THE MUST-JOIN EVENT FOR 2025 TRENDS.

🚀 What does market consolidation mean for venture capital in 2025?

Mercedes Bent, Venture Partner at Lightspeed, and Brian Murphy, Lead Data Scientist at Salesforce Ventures will share their perspectives with Affinity in an exclusive webinar on May 8.

As the investment landscape shifts, they'll break down key dealmaking trends, what top firms are doing differently, and how to position your firm for success.

Don’t miss this chance to gain exclusive insights. Register now →

📃 QUICK DIVES

1. Founders: stop saying these things in VC meetings.

Most founders waste their time in VC pitches—even VCs don’t want to hear half the stuff they say. So here are a few things I always suggest not saying in a pitch:

There's this classic line I keep hearing in pitch meetings: "We're aiming for a $20M–$100M exit to BigCo in a few years."

Look, it might be your genuine game plan, and there's nothing wrong with that. But here's the thing – most VCs will mentally check out the moment you say this. Why? Because those numbers just don't move the needle for their fund returns.

Plus, you're telling them you're building to sell, not to become massive. Even if that's your real plan, it comes across as thinking too small.

“We’re a bit burnt out after doing this for years.” I feel you. But say this to a VC, and that’s not a sign of founders they want to invest in for the next 5–10 years.

“We need the money to get sales and marketing going.” While logical, again, this isn’t what VCs want to hear. They want to hear you already have at least a tiny core revenue engine going, and the capital is going to feed it. Don't start it.

“Our CTO is leaving.” Important to know. Disclose it. But have a plan in place to address it before you pitch VCs.

“We need a lot of money because our burn rate is pretty high.” It’s not the VCs’ problem if your burn rate is too high. You need to make sure your startup is at least structurally attractive to the VC fund you talk to. Bigger funds can fund bigger burn rates. But you still need to be structurally attractive.

“I don’t know all that much about that key competitor.” The best founders always know the competition is cold. And respect it.

“Our sales are flat but we’ll make it up later in the year.” Prove it. This isn’t the risk VCs want to take.

“Our market is pretty small.” That’s OK if you have some proof you are going to expand it. E-signatures were a $1m a year market when we started Adobe Sign / EchoSign. Today, they are a $3B+ market. But you need to show a clear path for your small market to become a very large one.

“Our product wins because it costs less than the competition.” This rarely wins in SaaS, at least not big. It’s not an enduring competitive advantage.

“Oh those aren’t customers, they’re trials.” Be very careful exaggerating metrics. Don’t count trials as customers. Don’t count deals that haven’t quite closed yet … as closed. Don’t blend 3 months of revenue into “Quarterly MRR” to make your revenue look bigger.

You’ll likely get caught. And worse, maybe it wouldn’t have mattered at all to the VC if you’d been honest and clear up-front.

2. Do Early-Stage startups need a financial model for fundraising?

When you learn about entrepreneurship in school you’re taught to have a clear, strong business plan and financial model when you start out, and to use that as a way to communicate the path your business will take.

The real world is much messier. Any plan you had when you started gets changed quickly. Every day or even hour of your time that you devote to your startup needs to be spent getting it off the ground.

The same is true for a financial model. Your projections will be wildly wrong.

Not only that, but the levers you have at your disposal in the model may not end up being what you think they’ll be — the entire business may change, and you likely don’t know enough yet at the pre-seed stage to be sure.

Investors all know this. They see tons of startups and have many first-hand data points showing that everything can change and often does. What they don’t know is if YOU know that.

Investors are looking to de-risk the idea of investing in you. Startups are inherently so risky that they look for ways to think of your startup as less risky than others. One of those ways is to assess your founder mindset — how much do you “get” what being a founder will really be like?

The thinking there is that the more you “get” it the more you’ll be able to anticipate challenges and be emotionally steady when things get rocky.

This is a very common place where first-time founders and founders who don’t have a strong network fail to build trust with an investor. That might not be fair, but it’s true. Two of those signals for how well someone is ready to be a venture-backed founder are:

How well do they know how to prioritize their time?

Whether they realize everything will change from their “plan” or not. Presenting investors with detailed financial projections at the pre-seed stage fails both of those tests.

Ok… So Why is a Financial Model Useful?

VCs who want to see a model use it as a proxy for understanding whether a founder can correctly break down the incentives and value levers in a problem space.

VCs want to trust that if the business needs to change, the founder will be able to quickly figure out how to evaluate new opportunities and position their product for success in a new market. It's just a different way of de-risking an investment opportunity.

The simple takeaway is that each investor is different in what traits they value and how they reach conviction. So Know your investor - talk to their backed founders, and read their content. Think about the type of investor you want as a partner based on their evaluation approach.

You can download the financial model Excel template here.

3. Don’t price your product based on costs, why?

Founders often struggle with pricing their products correctly early on. Many make the mistake of setting prices based on their costs, especially in non-software startups. While this might seem logical, it's not the best approach. Here's why you should consider "unreasonable" pricing instead:

The Problem with Cost-Based Pricing

It doesn't account for the value you're providing to customers.

It can limit your growth potential and ability to invest in improving your product.

It may attract price-sensitive customers who aren't your ideal target market.

The Benefits of "Unreasonable" Pricing

Identifying Your Ideal Customer Profile (ICP)

High initial prices help you quickly identify customers who feel the pain point most acutely.

These customers are willing to pay more for a solution, even if it's not perfect yet.

Validating Market Demand

If people are willing to pay a premium, it confirms there's a strong need for your product.

This validation can save weeks of experiments and help you focus on the right target audience.

Accelerating Product Development

Higher initial revenue allows you to invest more in improving your product faster.

You can build specifically for your ICP, ensuring product-market fit.

Real-World Example

I see a lot of founders launch a website, with:

A logo that was just an emoji

An onboarding flow using Typeform

A database in Airtable

Also, set the initial price on the higher end. Despite this - they have seen good outcomes of getting a few people onboard 5-6, why? They felt the pain point so strongly that they wanted it solved at all costs.

The Inverse Relationship

There's an inverse relationship between how painful a problem is and how "perfect" the product needs to be:

More painful problem = less perfect product + higher willingness to pay

Less painful problem = needs to be perfect + price sensitivity

When to Launch

Once your product is 70-80% ready for your ICP, they will likely convert. If not, it may indicate that the problem isn't worth investing more time into, as the product will be hard to grow.

Long-Term Strategy

While starting with "unreasonable" pricing can be beneficial, it's important to note that this approach isn't permanent. As you grow and expand your market, you may need to adjust your pricing strategy. However, the initial high pricing helps validate the market, identify your ICP, and provide capital leverage for faster growth.

Remember, don't let perfect be the enemy of good. If you're solving a truly painful problem, your early adopters will be willing to pay a premium for an imperfect solution.

Even in one of the previous writeups, we have shared 5 frameworks that can help you to find the best pricing strategy for your startup.

THIS WEEK’S NEWS RECAP

🗞️ Major News In Tech, VC, & Startup Funding

New In VC

Revent, a Berlin-based VC focused on “planetary and societal health,” has closed a €100M ($109M) Fund II to back climate, healthcare, and economic empowerment startups. (Read)

Major Tech Updates

OpenAI plans to cut Microsoft’s share of its revenue from 20% to 10% by 2030, according to investor documents cited by The Information. (Read)

Google has released Gemini 2.5 Pro Preview (I/O edition), an upgraded AI model now available in the Gemini API, Vertex AI, AI Studio, and Gemini chatbot app. (Read)

Hugging Face has launched Open Computer Agent, a free cloud-hosted AI agent that operates a Linux VM and can perform simple computer tasks via apps like Firefox. (Read)

OpenAI has reversed its plan to become a full for-profit entity and will instead transition its business arm into a public benefit corporation (PBC), controlled by the original nonprofit. (Read)

OpenAI has agreed to acquire AI coding tool Windsurf (formerly Codeium) for around $3 billion, marking its largest acquisition to date, according to Bloomberg. (Read)

New Startup Deals

NewLimit, a San Francisco-based biotech startup founded by Coinbase CEO Brian Armstrong focused on extending healthy human lifespan through cellular reprogramming, raised $130M. (Read)

Rentana, a NYC-based AI-driven revenue intelligence platform for multifamily owners and operators, closed a nearly $5m seed funding round. (Read)

Onebeat, a NYC-based provider of a dynamic inventory optimization and execution platform, raised additional $15M in funding. (Read)

Tesseral, a San Francisco, CA-based authentication infrastructure for B2B software companies, raised $3.3M in Seed funding. (Read)

Recraft, a San Francisco-based AI image generator startup, raised $30M in a Series B round led by Accel. (Read)

→ Get the most important startup funding, venture capital & tech news. Join 45,000+ early adopters staying ahead of the curve for free. Subscribe to the Venture Daily Digest Newsletter.

TODAY’S JOB OPPORTUNITIES

💼 Venture Capital & Startup Jobs

All-In-One VC Interview Preparation Guide: With a leading investors group, we have created an all-in-one VC interview preparation guide for aspiring VCs, offering a 30% discount for a limited time. Don’t miss it. (Access Here)

Ecosystem Growth Associate - Motion Venture | Singapore - Apply Here

Associate - Rev1 Venture | USA - Apply Here

Investor (AI) - Samsung Next | USA - Apply Here

Senior Associate - Disrupt | UAE - Apply Here

Chief of Staff - First Round Capital | USA - Apply Here

Office Manager - Wind Ventures | USA - Apply Here

Venture Investments Associate - GSR | USA - Apply Here

Executive Assistant TCV | UK - Apply Here

Writer - First Round Capital | USA - Apply Here

Venture Scout - Sentiera Venture | USA - Apply Here

Associate - Aartha Venture Fund | USA - Apply Here

Analyst - Scope Venture | USA - Apply Here

Principal - Aartha Group | India - Apply Here

Partner - Chan Zuckerberg Initiative | USA - Apply Here

Venture Fellows - Kalea Venture | UK - Apply Here

Investor (AI) - Samsung Next | USA - Apply Here

Venture Scout - First Momentum Venture | Remote - Apply Here

Visiting Investment Analyst - Vorwerk Ventures | Germany - Apply Here

🔴 Share Venture Curator

You currently have 0 referrals, only 5 away from receiving a 🎁 gift that includes 20 different investors’ contact database lists - Venture Curator

The discussion about "unreasonable" pricing is fascinating. I've seen many startups struggle with pricing, and your point about the inverse relationship between problem pain and product perfection is particularly insightful.

I wonder about the transition from initial high pricing to a more sustainable pricing model. How do you suggest founders approach this shift without alienating early adopters?

The framework for thinking about runway is incredibly valuable, especially the distinction between net cash and gross cash positions. I've been through several funding rounds, and your point about runway being tied to milestones rather than just a number is spot on.

I'm curious about how you suggest handling venture debt in runway calculations. Do you think it's better to secure a line of credit early as a safety net, or should founders focus on equity funding first?